Our Take on Dave Ramsey's Baby Steps (With some Modern Twists)

The FreeBudget Team

The FreeBudget Team

📚 Who Is Dave Ramsey?

If you’ve ever Googled “how to get out of debt” while ugly crying over your bank account, chances are you’ve stumbled across a very serious man named Dave Ramsey.

Dave is a radio host, best-selling author, and one of the most recognized names in personal finance. He built a brand empire around helping people get out of debt, build wealth, and scream “I’M DEBT FREE!” on his show like it's a rite of passage. In the 1980s, Dave filed for bankruptcy after losing millions in real estate. Oof. But instead of disappearing into financial oblivion, he rose from the ashes like a very frugal phoenix. The result? The 7 Baby Steps: his step-by-step financial plan to financial peace.

Since then, Ramsey has become a household name in personal finance, especially popular with older Millennials, Boomers, and anyone who’s ever had a bad relationship with a credit card. But how do his ideas hold up for Gen Z and younger Millennials in 2025?

Let’s break it down.

And before we start - let’s make it clear that Dave is incredibly entertaining and has helped a LOT of people. Our modern twists on his tried-and-true system aren’t meant to detract from the principles themselves, but rather to make it relevant to you youngins. If you’re not from the south and don’t know what a youngin is, we’ll save you the google search - its a “young one.”

👶 The 7 Baby Steps (a.k.a. Dave’s Money Rules of Life)

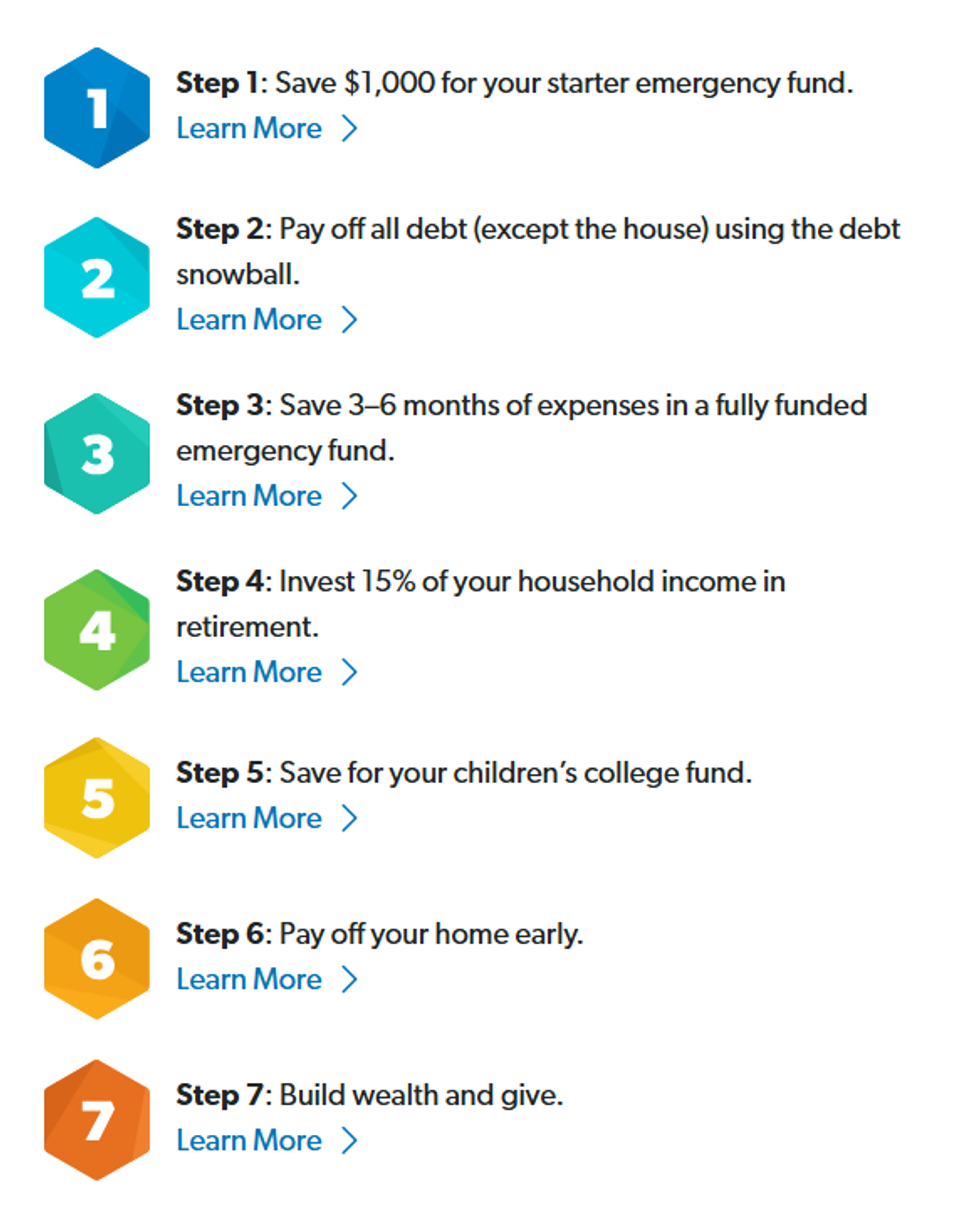

< This infographic is a screenshot from Dave’s website - we take no credit. Check out ramseysolutions.com for more information on each step.

Baby Step 1: Save $1,000 for Your Starter Emergency Fund

📍Emergency funds are like your financial seatbelt.

This is your “oh no” money: car repairs, surprise bills, or when your dog eats an AirPod. It’s not a lot, but it’s supposed to keep you from reaching for that high-interest credit card every time life throws a wrench at you.

👉 FreeBudget's Take: We totally agree with Dave. You need to find $1,000 as soon as possible and this is an easy psychological win to get the momentum rolling. Nuff saaid.

BUT… might we add our own “Baby Step 1.5” before we move to the debt snowball?

FreeBudget’s Baby Step 1.5: Track (and Cut) Your Expenses. It’s going to be SO much easier to pay your debts efficiently–and move through the rest of Dave’s Baby Steps - when you have an eye on every single card swipe. Every single transaction. You have no idea what expenses you can cut, and how much, until you do this. It will change your life, if we dare say so ourselves. That’s why we’ve created a tool to help you do this well. Once you’ve trained yourself to track expenses and slash them a Fruit Ninja pro, you’ll be set up perfectly for Step 2.

Step 2: Pay Off All Debt (Except the House) Using the Debt Snowball

📍Per Dave - List your debts smallest to largest. Pay off the smallest one first.

This one’s controversial. Ramsey says ignore the interest rates; just knock out the smallest debts first to build momentum. And on one hand, we get it. But…

👉 FreeBudget’s Take: Dave’s approach here works very well for people who are initially struggling to be motivated to pay off debts. Smaller debts feel more manageable – and naturally, we’ll feel a motivation boost when we pay them off. However, for anyone looking to slash debt efficiently and ASAP, there’s a better approach. Tackling debts from the largest interest rate to the smallest interest rate is going to ultimately save you more money in interest fees and help you get out of debt quicker. The approach you choose to take should be based on what motivates you and which plan you can stick to.

Step 3: Save 3–6 Months of Expenses in a Fully Funded Emergency Fund

📍Now we’re stacking serious cash.

Once your debts are gone (yay!), the idea is to build a real buffer. This protects you from job loss, economic chaos, or when your entire apartment floods because your upstairs neighbor doesn’t understand plumbing.

👉 FreeBudget’s Take: Yes, yes, yes. Three to six months is the perfect buffer amount. If you want to sleep well at night, supplement the magnesium sprays with a fully-funded emergency fund. You’ll wake up with enough energy to run through a brick wall. If you follow our Baby Step 1.5 and cut your monthly expenses early on, that’ll lower the amount you need to save here.

Step 4: Invest 15% of Your Household Income into Retirement

📍Invest in 401(k)s, Roth IRAs, and whatever your job gives you.

Ramsey loves long-term investing. He’s super into mutual funds and doesn’t vibe with crypto or trendy investing. This step is all about starting early and letting compounding do the work.

👉 FreeBudget’s Take: We’re tracking with you, Dave. Skip the crypto and speculative investments – really anything that sounds too good to be true. We would add that utilizing a broad-based index fund, such as an S&P or Total Stock Market Index Fund, is a diversified and reliable investing strategy. No need for frills. We’d also add that there’s no reason to cap this at 15% if you’re able to invest more. If you’re interested in the FIRE movement (Financial Independence, Retire Early), your investing goal should be significantly higher than 15%. Nearly half of American households had *ZERO* savings in retirement accounts in 2022, according to the Survey of Consumer Finances. Anything you can save is better than zero.

Step 5: Save for Your Children’s College Fund

If you’ve got kids (or want them), now’s the time to start thinking about their future student loans - or ideally, lack of them. Millennials and Gen Zers are all too familiar with the ridiculous cost of a college education. This Baby Step shouldn’t be taken lightly.

Ramsey recommends ESAs or 529 plans. But how much should you save?

👉 FreeBudget’s Take: Despite popular opinion, we don’t believe everyone should go to college. Certain careers really do need a college degree, but many don’t. If you spent Baby Step 2 trying to pay off your own student loans, you’re probably really determined not to have history repeat itself with your kids. So, here’s what we’re doing (and what we recommend for you). Decide on a set amount of money that you’d like to work toward saving for education. Keep in mind that your child can:

- Take some college classes in high school to fast track a college degree

- Do a year or two at a technical college to get general education credits done for less

- Pursue scholarship opportunities or work study programs

- Participate in high school career center programs that can turn into reliable full-time work

- Be a resident assistant (RA) or live at home to save on housing

- …and you can always split the financial burden with your child as well, if they choose to pursue an expensive program or specialized field of study! It may actually teach them a thing or two about money!

Considering the possibilities, maybe you decide not to save for a full four-year degree. Maybe you aim to save half, leaving room for some other options. Then, determine how much money you’d need to contribute to a 529 per month in order to hit that number.

Step 6: Pay Off Your Home Early

📍No more mortgage. Zero. Nada. Clean slate.

This is the step where people start flexing. Ramsey says once you’ve taken care of everything else, it’s time to throw extra money at the mortgage until it’s gone. Because “debt-free” includes your house too.

👉 FreeBudget’s Take: It is increasingly difficult to own a home to begin with. If you’re one of the lucky ones with a low mortgage rate, you may decide that it’s better NOT to pay off your home early. Instead, you can invest the money you would’ve put toward your mortgage (see Step 4) and make more in the market than you would make by paying off your home early. However, if you bought a house in the last few years with a 6 or 7% interest rate, we’d proceed with this Baby Step and pay off the mortgage.

Step 7: Build Wealth and Give Generously

📍You made it. Now be a baller (responsibly).

This is the “financial zen” stage. You’ve got no payments, no stress, and you’re giving generously - whether that’s to family, community, or causes you care about. You’re living the dream.

👉 FreeBudget’s Take: There really is no better feeling than being able to meet tangible needs for others. We would argue that giving generously should be woven into your financial picture before this stage, wherever possible. However, at Baby Step 7, you’ll be able to give like never before - especially if you’re using FreeBudget to help you keep expenses low and budget like a boss.

🧠 So… Does This Still Work for Everyone in 2025?

Short answer? Mostly.

Long answer? Yes, but with some edits.

Ramsey’s system is beautifully simple, and that’s why it works for so many people. But let’s be real: the economy today is not the economy of 1995. Gen Z is juggling:

- Sky-high rent prices

- A gig economy

- Wild student loans

- And the general stress of trying to afford therapy and oat milk

That’s where a little modern budgeting magic comes in.

💸 How FreeBudget Can Help You Do the Baby Steps (Without Losing Your Mind)

Whether you’re trying to save your first $1,000 or figuring out how to escape the quicksand of student loans, FreeBudget was designed to help you make sense of your money without charging you a dime. Here's how we help:

- 📊 Visual goal tracking: Watch your debt shrink or your emergency fund grow. Motivation: unlocked.

- 📈 Real-time budget insights: Know what’s coming in, what’s going out, and how close you are to your next Baby Step.

- 🧠 Financial literacy tips baked in: We don’t just show you your numbers; we help you understand them.

It’s 2025. You shouldn’t need a spreadsheet degree or $100/month to build a budget. You just need FreeBudget - your financial sidekick that’s as modern as you are.